What do you do when you have a client with debt problems and your business model does not include budgeting and debt management advice? Do you ignore it and hope for the best, or do you make an exception and offer budgeting and debt management advice?

The Problem With Ignoring Client Debt

When clients owe money on credit cards or other forms of consumer debt, it can be difficult to follow any recommendation that requires additional financial commitment. For many, if they implement your advice, they may end up making only minimum payments. When this happens, it can take 25 or more years to pay off their debts and cost thousands in interest. Money that could be better used to protect their family and save for retirement.

So, what are your options if you do not want to ignore their debts and you do not want to add budgeting and debt management to your service offering? You educate clients to help themselves.

Wilfred’s Story

Wilfred was referred to you by a loyal client of yours, his parents. He is 30 years old and has been paying interest on consumer debt for over 10 years, ever since borrowing $1,000 for a big screen TV. Last year he received an offer from a well-known financial institution to consolidate all his credit card debts. The annual rate of interest was only 0.99% for the first year, plus a 1.5% upfront fee. Wilfred liked the interest rate and was sure he could pay off all his debts before the regular cash advance rate kicked in. He was wrong!

In addition to not paying off the consolidated debt, he added new debts and currently owes $20,000 as follows:

- $3,500 on a car loan at 6.9% interest

- $4,500 on a gaming computer at 19.9%

- $12,000 on the consolidated credit card at 24.9%

Tired of living paycheque to paycheque, he asked his parents for some advice, and they suggested he talk with you, their trusted financial advisor. You arrange a virtual meeting with Wilfred where he tells you he thinks he can pay $650 each month to lower his debts. After congratulating him on taking the first step, you provide the following advice.

Freeze Your Debt

Before you can eliminate your credit card debt you have to stop using them, and the best way to do that is with a budget. A balanced budget can reduce unnecessary expenses so that each pay period you have excess money you can use to pay down debt.

To create a budget, you suggest to Wilfred that he use the Credit Canada Budget Planner.

Create a Payment Plan

If you only have one credit card, your plan is simple, use the excess money from your budget to pay down your debt. When you have multiple debts with varying interest rates, you need to allocate the excess money you have each month for maximum results.

You tell Wilfred about the Credit Canada Debt Calculator, a free online application that will calculate how long it will take him to be debt-free using 5 different repayment strategies, and how much he could save in interest.

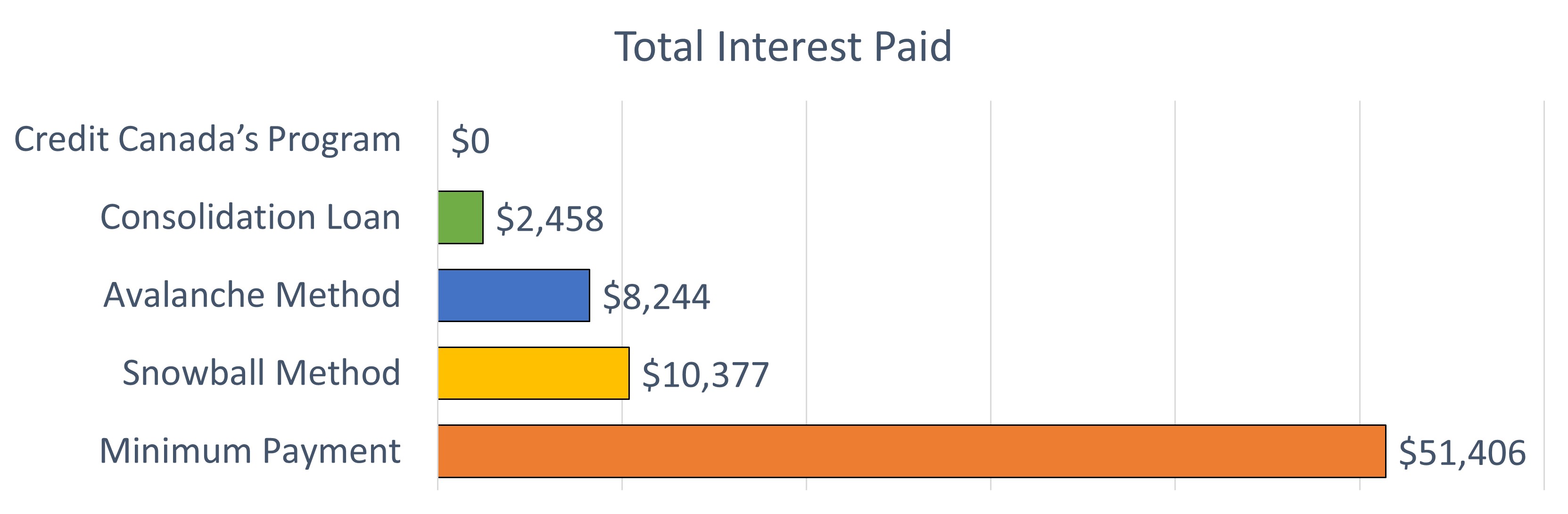

Credit Canada Debt Calculator Results

Minimum Payment

Making the minimum payment is what Wilfred has done for the past 10 years, costing him thousands in interest.

If Wilfred continues to make only minimum payments, it will take over 25 years to pay off his debt and cost $51,406 in interest.

The Snowball

With this method you focus on paying down the debts with the smallest balances first, while continuing to make minimum payments on your other debts. This provides a phycological advantage as small debts are eliminated.

Using the snowball approach, it will take Wilfred 3.9 years to pay off all his debts and cost $10,377 in interest. A savings of $41,029 in interest compared to making minimum payments.

The Avalanche

With this method, you focus on paying down the debts with the highest interest rates first, while continuing to make minimum payments on your other debts. This lowers over-all cost as the highest interest debts are eliminated first.

Using the avalanche approach, it will take Wilfred 3.7 years to pay off all his debt and cost $8,244 in interest. A savings of $2,133 in interest compared to the snowball method.

Consolidation Loan

With this method, you use your good credit rating to get a debt consolidation loan from your bank and roll all your debts into one easy payment. This will provide the best results, if you stop using your credit cards, and the worst result if you do not!

If Wilfred uses a consolidation loan with an interest rate of 8%, it will take 2.9 years to pay off his debt and cost $2,458 in interest. A savings of $5,786 in interest compared to the avalanche method.

Credit Canada’s Debt Consolidation Program

If your credit rating is not good and your bank turns you down for a debt consolidation loan, you can work with a credit counsellor at Credit Canada to set up a Debt Consolidation Program.

With this program, Wilfred will pay no interest and his monthly payments will be $463 for 4 years.

Summary

The avalanche method is the one Wilfred decided to use. It will help him pay off his debts in less than 4 years and save thousands in interest charges.

So why did he choose the avalanche method?

Wilfred has always paid his credit cards on time, so his good credit rating would not qualify him for Credit Canada’s debt consolidation program. He considered contacting his bank for a consolidation loan but decided against it out of fear he might start using his credit cards again.

Financial Management as a Value Add

Not every client will be as willing as Wilfred to do the work and help himself to budget and eliminate debt. In these situations, you may want to consider an easy-to-use solution where you can create a debt payment plan using the avalanche method.

If this is something your planning software lacks, checkout RazorPlan Financial Planning Software. With RazorPlan you can quickly create a report that compares your client’s current payment strategy to one that will save them thousands in interest.